Managing employees on digital nomad visas in the EU can be tricky. While these visas allow remote work in over 15 European countries, they come with legal and tax challenges for employers. Here’s what you need to know:

- Tax Residency Risks: Employees staying 183+ days in a country may trigger tax residency and expose your company to local corporate taxes.

- Permanent Establishment (PE): Remote work locations can create a taxable business presence, leading to corporate tax obligations.

- Labor Law Compliance: EU countries enforce local labor protections, like minimum wage, working hours, and social security contributions, even if contracts specify foreign laws.

- Social Security Contributions: Without an A1 certificate, employers risk double contributions or penalties.

- Visa Limitations: Digital nomad visas don’t guarantee full work authorization; some countries impose income source limits (e.g., Spain allows only 20% income from local clients).

To manage these risks:

- Use pre-approval checklists for location changes.

- Monitor employee work locations and visa conditions.

- Consider Employer of Record (EOR) services for compliance in specific countries.

- Stay updated on EU labor laws and tax rules.

The shift to stricter oversight, especially with the EU’s biometric Entry/Exit System, means employers must prioritize compliance to avoid fines, audits, or legal disputes.

The Gap Between Residency Rights and Employment Authorization

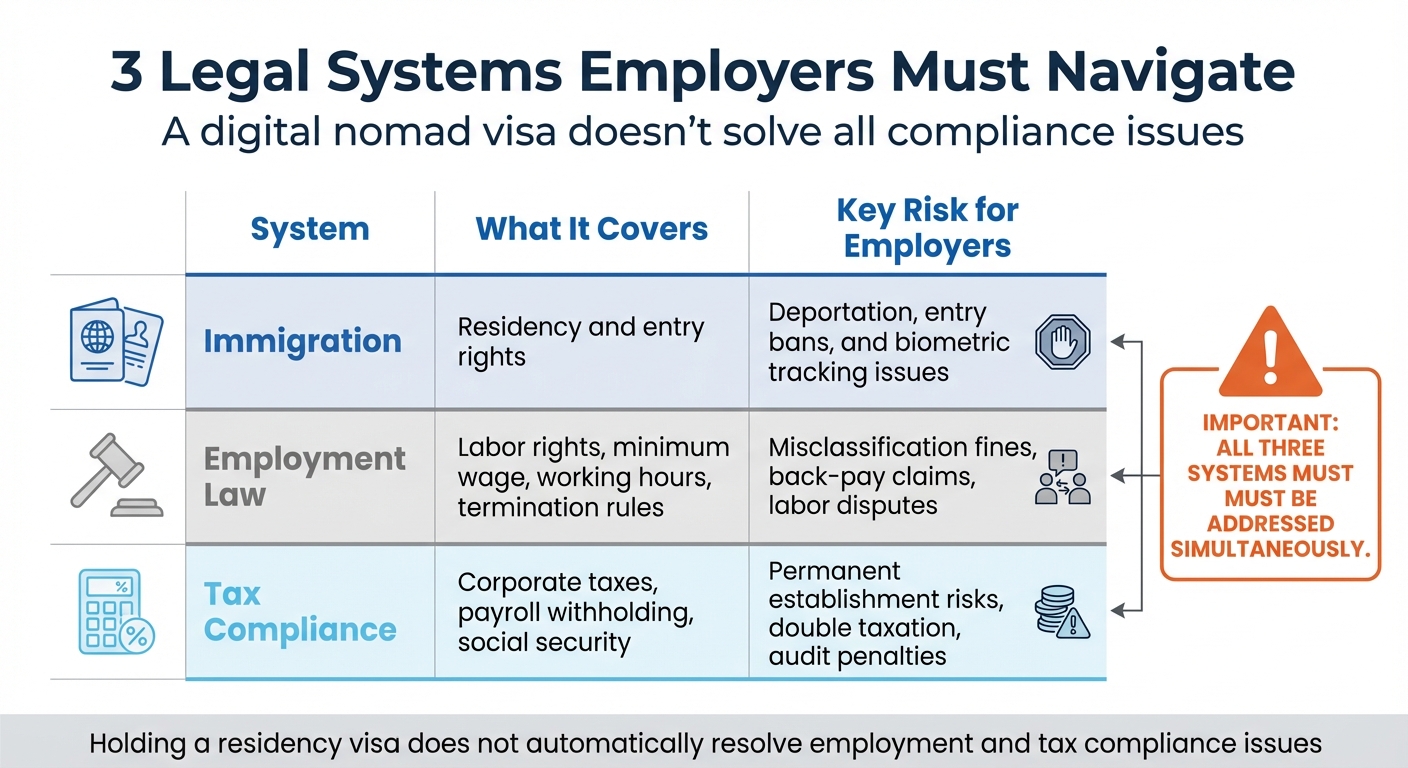

Three Legal Systems Employers Must Navigate for EU Digital Nomad Compliance

A digital nomad visa allows individuals to reside in an EU country but does not automatically grant local work authorization or provide tax exemptions.

Common Misconceptions About Digital Nomad Visas

Even with the distinction between residency and work rights clarified, many employers mistakenly assume that a digital nomad visa ensures full legal compliance. In reality, these visas primarily prevent deportation for overstaying. For instance, Spain’s digital nomad visa allows holders to earn up to 20% of their income from Spanish clients, while the remaining 80% must come from foreign sources. If this ratio is exceeded, the individual risks penalties for non-compliance.

"Contract choice of law cannot override mandatory local employment protections." – Yousign

Another frequent misunderstanding is that the visa suspends time limits across the European Union. A Type D long-stay visa only exempts the holder from the 90/180-day rule within the issuing country. If the individual travels to other Schengen states, the 90-day limit still applies. Adding to this complexity, the EU’s biometric Entry/Exit System ensures strict monitoring and enforcement of visa conditions.

These examples highlight the importance of understanding the various legal frameworks at play.

3 Legal Systems Employers Must Navigate

Employers need to recognize that holding a residency visa does not automatically resolve employment and tax compliance issues. They must address three distinct legal systems:

| System | What It Covers | Key Risk for Employers |

|---|---|---|

| Immigration | Residency and entry rights | Deportation, entry bans, and biometric tracking issues |

| Employment Law | Labor rights, minimum wage, working hours, termination rules | Misclassification fines, back-pay claims, labor disputes |

| Tax Compliance | Corporate taxes, payroll withholding, social security | Permanent establishment risks, double taxation, audit penalties |

Even when a visa is valid, the employee’s activities might create a "taxable presence" in the host country, which could expose the employer to corporate tax obligations. These challenges go beyond immigration and touch on employment and tax law compliance, making it essential for employers to navigate these overlapping systems carefully.

sbb-itb-e5b9d13

Employment Law Risks: Local Requirements and Obligations

When a digital nomad works in an EU country, local labor laws take precedence – no matter what the employment contract states. According to the Rome I Regulation, the employment relationship is governed by the laws of the country where the employee "habitually works." This means a U.S. company cannot simply enforce American labor standards for an employee working remotely in Spain or Germany, even if the contract specifies U.S. law. This creates a compliance minefield for employers, adding to the immigration and tax hurdles already mentioned. Local regulations impose specific obligations that often differ sharply from U.S. norms, setting the stage for the requirements outlined below.

Required Employment Protections

EU labor laws impose non-negotiable protections, regardless of contract terms. These include minimum wage laws, limits on working hours, mandatory rest periods, annual leave entitlements, and termination notice requirements. For instance, paid leave in Europe typically ranges from 20 to 30 days per year, excluding public holidays. This is far more generous than what most U.S. companies offer.

Social security contributions operate under the "pay where you work" principle. Unless the employee has an A1 certificate confirming coverage in another country, employers are required to contribute to the local social security system where the employee is physically working. These contributions provide access to benefits such as healthcare, pensions, unemployment support, maternity/paternity leave, and sick pay.

While these protections apply broadly across the EU, enforcement and additional requirements vary significantly by country.

How Labor Laws Differ Across EU Countries

The enforcement of labor laws and specific requirements can differ greatly between EU nations. Countries like France, Germany, and Spain are known for their particularly stringent regulations.

- France: Employees are governed by the French Labour Code, which mandates occupational accident insurance – even for remote workers.

- Germany: Employers must document remote work hours in writing and, for larger teams, consult with works councils.

- Spain: Remote work exceeding 30% of total hours requires a specific written agreement, and payroll must be processed through a local entity or agent.

Other countries have their own unique rules:

- The Netherlands: Employees have a statutory right to request flexible or remote work and are entitled to an 8% holiday allowance (vakantiegeld) in addition to their salary.

- Portugal: Employers must reimburse remote workers for costs like electricity and internet.

These country-specific rules demand customized compliance strategies for each location.

Misclassification is another major risk area. For example, in October 2024, Massachusetts reached settlements with Uber Technologies and Lyft Inc., requiring the companies to pay $148 million and $27 million respectively over claims that drivers were misclassified as independent contractors instead of employees. Similarly, EU countries aggressively enforce rules against "false self-employment", with penalties that can include retroactive social security contributions and hefty fines.

Tax Liabilities and Permanent Establishment (PE) Risks

Tax obligations add another layer of complexity for employers managing remote teams. The rule is straightforward but often overlooked: employers must handle payroll taxes in the country where the employee physically works. This principle, known as lex loci laboris, means adhering to the laws of the work location.

Payroll Obligations and Withholding Taxes

When a digital nomad is working in Spain, Germany, or any EU country, the employer is responsible for local payroll tax withholding from the very first day. For U.S. companies, this means registering with the host country’s tax authority, calculating taxes based on local brackets, and following the required payment schedule. Employers must also comply with local labor laws, including minimum wage and statutory benefits. For instance, in the Netherlands, employers are required to pay a holiday allowance (vakantiegeld) of at least 8% of the employee’s salary. These obligations apply even if the employer has no physical office in the country. Beyond payroll taxes, businesses must also be mindful of broader corporate tax challenges, particularly permanent establishment risks.

Permanent Establishment Risks

Payroll tax duties might be immediate, but the risk of creating a permanent establishment (PE) for corporate tax purposes is much more significant. A permanent establishment refers to a taxable business presence in a host country, which traditionally required a physical office. Now, even remote work locations can meet the criteria for PE exposure.

The 2025 OECD guidance outlines a three-step test to assess PE risks:

- Is the location, such as a home office, used on a permanent basis?

- Does the employee spend at least 50% of their working time there over 12 months?

- Does the employee’s presence directly contribute to business operations, like managing local clients or covering specific time zones?

"If the worker’s location materially enhances service delivery, such as through time-zone coverage, PE exposure can arise even without local clients or physical meetings." – Express Global Employment

Senior employees pose a heightened risk. For example, if a sales director or executive negotiates or finalizes contracts while working remotely in an EU country, this could trigger an "Agent PE." This would subject the company to corporate taxes on profits linked to that presence. The fallout includes corporate tax registration, VAT compliance, transfer pricing obligations, and penalties for retroactive non-compliance.

Social Security Contributions

Social security contributions follow the same "pay where you work" rule as income tax. Under EU Regulation 883/2004, employees are subject to the social security laws of the country where they physically perform their work. Contribution rates vary widely across countries: France charges around 67% (combined employer and employee), Spain approximately 36.9%, Germany about 40%, and Ireland roughly 15.05%.

To avoid double contributions, A1 certificates are essential. These documents confirm which social security system applies to a worker and are especially important for temporary cross-border arrangements. However, starting July 1, 2024, retrospective A1 certificates can only be issued for up to three months prior to the application date. The EU Framework Agreement on Telework (effective July 2023) provides some relief, allowing employees to stay within their employer’s social security system if they spend less than 50% of their time working in their country of residence. Without proper A1 documentation, employers risk dual social security liabilities and potential audits.

How to Reduce Risks: A Compliance Framework

Managing legal risks in EU digital nomad setups requires a structured approach that addresses immigration, employment, tax, and operational obligations. A proactive system can help mitigate these risks before they become significant issues.

Pre-Approval Checklist for Digital Nomad Arrangements

To tackle compliance challenges effectively, a pre-approval checklist can serve as a key tool for risk management. Employees should submit location change requests at least 30 days in advance, and the checklist should cover the following six areas:

- Legal work status and labor laws: Confirm a valid Digital Nomad Visa and determine which country’s labor protections apply under the Rome I Regulation.

- Tax and payroll assessment: Evaluate risks of permanent establishment and ensure registration for local payroll taxes, if required.

- Social security coordination: Obtain an A1 certificate to avoid double contributions.

- Data security protocols: Ensure the use of GDPR-compliant VPNs and secure data handling practices.

- Occupational health and safety: Verify that the home office meets essential safety requirements.

It’s critical for employers to include approved work locations in employment contracts. Working on a tourist visa is generally illegal in most EU countries and can lead to hefty fines. Additionally, contractual "choice of law" clauses cannot override mandatory local rules, such as minimum wage, working hours, or termination protections.

Using Employer of Record (EOR) Solutions

For smaller teams (1–10 employees per country), an Employer of Record (EOR) can be a cost-effective alternative to setting up a local legal entity, which can run between $50,000 and $150,000+ annually per jurisdiction. An EOR acts as the legal employer in the host country, managing tasks like payroll, tax withholdings, and social security contributions. This setup helps shield your business from being classified as having a taxable presence abroad.

EOR services typically charge 10–15% of an employee’s gross salary or a flat fee of $300–$800 per month per employee. Leading providers include Remote.com (which owns its entities), Deel (offering tools for contractor-to-employee conversions), and Oyster HR (with built-in salary benchmarking). When choosing an EOR, confirm entity ownership in complex markets like Germany, France, or Spain to ensure accountability during tax audits or labor disputes. Note specific challenges in Spain, where EOR contracts may not qualify for Digital Nomad Visa applications, and in Germany, where temporary agency work is capped at 18 months, necessitating a clear exit or transition plan.

While EOR solutions simplify compliance, continuous oversight remains a necessity.

Regular Compliance Monitoring

Ongoing monitoring of visa conditions, tax residency, and labor laws is essential. Employers must track where employees are physically working to maintain visa compliance and proper tax treatment. The 183-day rule is particularly important – spending more than 183 days in a country usually triggers individual tax residency, resulting in additional withholding obligations.

To stay compliant, employers should:

- Track work locations and verify authorization.

- Audit local compliance for minimum wage, leave entitlements, and other labor protections.

- Assess risks of permanent establishment.

- Regularly review VPN usage and ensure secure data handling.

Employment contracts should be updated whenever an employee changes their primary work location, as local labor protections will take precedence over existing terms. A formal digital nomad policy is also recommended, outlining limits on stay durations, equipment standards, and required notification periods for location changes.

"Remote gives me a lot of peace of mind that wherever we want to hire someone, it works, and we’re doing exactly everything by the book" – Jochem van der Veer, CEO & Co-Founder of TheyDo

Regular audits are vital since EU labor laws are always evolving – what works today may not be compliant tomorrow.

Conclusion

Hiring digital nomads within the EU comes with a web of legal challenges, far beyond simply ensuring visa compliance. Immigration violations, like allowing a digital nomad to overstay the Schengen 90/180-day rule, can lead to fines exceeding €1,000 and even multi-year entry bans for employees. On top of that, misclassifying workers or neglecting payroll and social security obligations can result in hefty penalties for employers.

With the introduction of automated biometric tracking, these compliance issues are harder to overlook. The EU’s Entry/Exit System (EES), launching October 12, 2025, will use biometric data to instantly flag visa overstays, removing the ambiguity that once existed. Employers must also navigate the 183-day tax residency rule and the Schengen limits with precision – there’s no room for informal practices or guesswork anymore.

To manage these risks, companies need a well-structured compliance strategy. This might include tools like pre-approval checklists, localized employment contracts, A1 certificates to coordinate social security, regular tracking of employees’ work locations, and Employer of Record solutions for smaller teams. Together, these measures create a framework that balances flexibility with legal security.

The transition from informal "stealth" nomadism on tourist visas to formal Digital Nomad Visas marks a major shift in how remote work is regulated across Europe. Relying on outdated contracts or practices could lead to serious financial and legal consequences. Additionally, EU labor laws vary between member states and are subject to change, meaning compliance today doesn’t guarantee compliance tomorrow.

Employers need to adopt a proactive approach to managing digital nomad arrangements. Whether through in-house compliance teams, local legal advisors, or Employer of Record partnerships, treating these setups as complex cross-border employment relationships is essential. By doing so, companies can reduce legal risks while ensuring smooth and compliant remote work arrangements.

FAQs

When does remote work in the EU create a permanent establishment risk?

Remote work within the EU can lead to a permanent establishment risk for employers. This happens when an employee’s activities in a specific country create a taxable presence for the company. Key factors influencing this risk include the type of work being performed, the employee’s physical presence, and whether their activities generate substantial economic activity, as outlined by local laws and bilateral tax treaties. To steer clear of unexpected tax liabilities, employers need to carefully evaluate these conditions.

What should employers track to avoid tax residency and payroll surprises?

Employers need to keep an eye on how many days digital nomads spend in each country, carefully document their locations and work-related activities, and stay mindful of the 183-day threshold. This is crucial to avoid unexpected tax residency complications or payroll issues. Maintaining thorough records not only ensures compliance but also minimizes potential legal risks.

Do digital nomad visas let employees work for local EU clients legally?

Digital nomad visas generally permit individuals to work remotely for clients located outside the EU. However, taking on work for local clients within the EU often comes with extra legal and regulatory hurdles. This can include adhering to specific labor laws and tax regulations in the country where the work is being performed. Employers must carefully navigate these requirements to remain compliant and mitigate any potential legal or financial risks.